Kenya’s Pension Sector: Fewer Schemes, Massive Asset Growth

Abstract

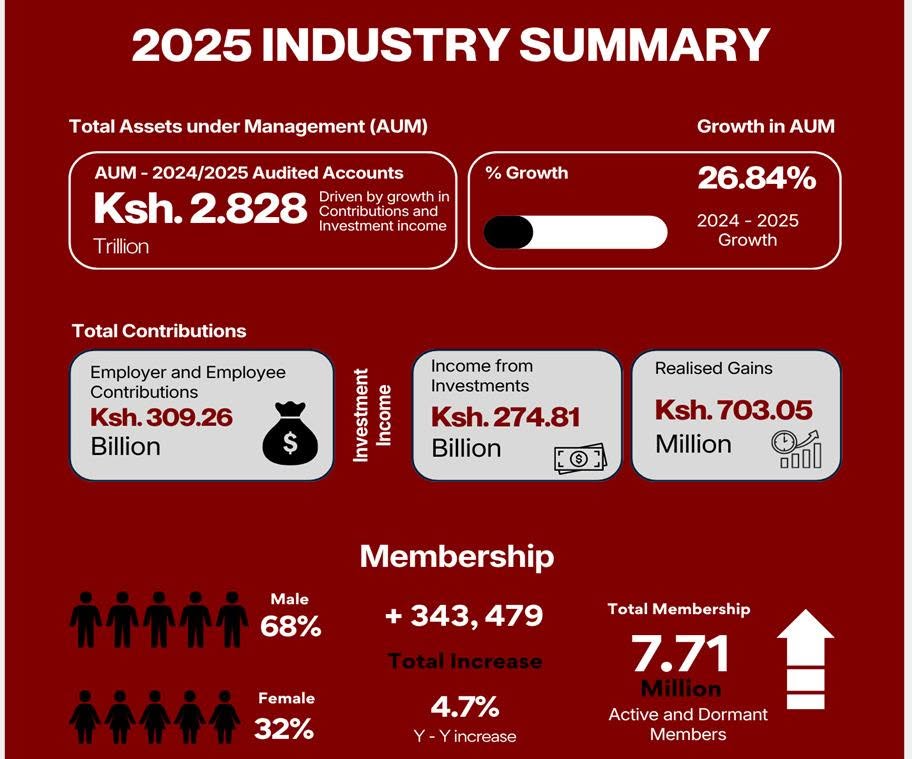

Kenya's retirement benefits sector is experiencing a significant transformation, marked by a paradox: a shrinking number of individual pension schemes alongside a massive surge in assets under management (AUM). Latest data from the Retirement Benefits Authority (RBA) indicates that pension assets reached KSh 2.81 trillion by December 2025, reflecting a robust 24.57% year-on-year growth. This expansion is primarily driven by legislative reforms, particularly the National Social Security Fund (NSSF) Act, 2013, favourable macroeconomic conditions, and strong investment performance. Concurrently, the industry is witnessing a consolidation trend, with smaller schemes merging into larger, more efficient umbrella funds, driven by the need for economies of scale, enhanced governance, and improved compliance. This article delves into the legal and regulatory underpinnings of these trends and their implications for practitioners.

Introduction

The Kenyan retirement benefits sector is undergoing a profound structural shift, presenting both opportunities and challenges for legal professionals and scheme stakeholders. Recent reports from the Retirement Benefits Authority (RBA) highlight a compelling dichotomy: a noticeable reduction in the absolute number of registered pension schemes, juxtaposed with an unprecedented growth in the sector's total assets under management (AUM). This dual trend signifies a maturing industry, driven by a complex interplay of regulatory reforms, economic dynamics, and strategic consolidation efforts.

By December 2025, Kenya's pension assets had swelled to an impressive KSh 2.81 trillion, marking a substantial increase from previous periods. This financial expansion is not merely organic but is significantly propelled by legislative interventions, such as the phased implementation of the National Social Security Fund (NSSF) Act, 2013, which has broadened the contribution base and increased limits. Simultaneously, the observed consolidation of schemes, particularly into umbrella funds, reflects a strategic response to rising administrative costs, the demand for improved governance, and the pursuit of economies of scale. This article will explore the statutory and regulatory framework governing these developments, analyse the drivers behind the asset growth and scheme consolidation, and discuss the practical implications for legal practitioners navigating this evolving landscape.

Background

The regulatory framework for Kenya's retirement benefits sector is primarily enshrined in the Retirement Benefits Act, Cap 197 of the Laws of Kenya (the "Act"). Prior to its enactment in 1997 and the subsequent establishment of the Retirement Benefits Authority (RBA) in October 2000, the sector was largely unregulated, relying on fragmented legislation, mainly the Income Tax Act and general trust laws. This often led to inconsistent administration and significant risks to members' funds. The RBA was established with a clear mandate: to regulate and supervise the establishment and management of retirement benefits schemes, protect the interests of members and sponsors, promote the development of the sector, and advise the National Treasury on policy matters.

The Act distinguishes between various types of schemes, including Occupational Retirement Benefits Schemes (ORBS), Individual Retirement Benefits Schemes (IRBS), and Umbrella Retirement Benefits Schemes (URBS). Each type is governed by specific regulations, such as the Retirement Benefits (Occupational Retirement Benefits Schemes) Regulations, 2000, the Retirement Benefits (Individual Retirement Benefits Schemes) Regulations, and the Retirement Benefits (Umbrella Retirement Benefits Schemes) Regulations. These regulations set out detailed requirements for registration, administration, investment, and benefit payouts. The RBA's oversight ensures compliance with these provisions, fostering a stable and trustworthy environment for retirement savings. The historical lack of a centralized regulatory body underscored the necessity for the RBA, which has since played a pivotal role in shaping the sector's growth and stability.

Analysis

The observed trend of fewer schemes but massive asset growth in Kenya's pension sector is a multifaceted phenomenon, driven by both regulatory imperatives and market dynamics. The consolidation of schemes, particularly into umbrella funds, is a prominent strategy aimed at enhancing efficiency and stability. Smaller schemes often face disproportionately high administrative and investment costs per member. By pooling resources under umbrella schemes, which cater to multiple unrelated employers, these entities can achieve economies of scale, negotiate better terms with service providers, and streamline operations. This consolidation also leads to more robust governance structures, as larger schemes can afford specialized staff and implement sophisticated risk management strategies, ultimately benefiting members through improved oversight and decision-making.

Concurrently, the substantial growth in pension assets is attributable to several key factors. A major driver has been the phased implementation of the National Social Security Fund (NSSF) Act, 2013, which significantly increased contribution limits and expanded the overall contribution base. For instance, the lower earnings limit rose to KSh 8,000 and the upper limit to KSh 72,000, materially boosting long-term savings accumulation. Beyond statutory contributions, a supportive macroeconomic environment, characterized by stable inflation, a relatively stable Kenya Shilling, and easing interest rates, has fostered a favourable investment climate. Strong performance in capital markets, particularly the Nairobi Securities Exchange (NSE), has also contributed significantly to investment income and valuation gains, further propelling asset growth.

From a legal perspective, these trends necessitate careful attention to fiduciary duties and investment regulations. Trustees of pension schemes are bound by stringent fiduciary obligations to act in the best interests of members, including prudent investment of scheme funds. The Retirement Benefits Act, Cap 197, and its subsidiary regulations, such as the Retirement Benefits (Investment of Funds) Regulations, provide guidelines on permissible asset classes and diversification requirements. While the industry's portfolio remains heavily allocated to traditional assets like government securities (over 50%) and quoted equities, there is a growing push towards diversification into alternative investments.

Recent regulatory amendments also reflect the RBA's proactive approach to industry development. For example, the Retirement Benefits (Occupational Retirement Benefits Schemes) (Amendment) Regulations, 2021, and the Retirement Benefits (Umbrella Retirement Benefits Schemes) (Amendment) Regulations, 2021, introduced changes regarding access to benefits before retirement. Members leaving employment before early retirement age can now access up to 50% of their total accrued benefits, including employer contributions, a shift from previous rules. Furthermore, regulations have been introduced to prevent conflicts of interest by prohibiting trust corporations from appointing related service providers (administrators, fund managers, custodians). These amendments underscore the regulator's commitment to member protection and enhanced governance within the consolidating and expanding sector.

Conclusion

The Kenyan pension sector is undeniably on a trajectory of significant growth and structural evolution, characterized by a strategic consolidation of schemes and a remarkable expansion of assets. This dual trend, driven by robust regulatory frameworks, legislative reforms like the NSSF Act, 2013, and a favourable investment climate, points towards a more resilient, efficient, and professionally managed industry. The shift towards larger, often umbrella, schemes is a pragmatic response to the increasing demands for cost efficiency, enhanced governance, and stringent compliance, ultimately aiming to deliver better outcomes for members.

For legal practitioners, these developments present a dynamic landscape requiring continuous engagement with the evolving regulatory environment. Key implications include the need for meticulous due diligence in scheme mergers and consolidations, expert advice on investment governance and compliance with RBA directives, and a thorough understanding of the amended rules on benefit access and conflict of interest. As the RBA continues to refine its supervisory framework and promote sector development, practitioners must remain vigilant to emerging policy shifts and legislative amendments. The future of Kenya's pension sector promises further deepening and expansion, necessitating proactive legal counsel to navigate its complexities and harness its opportunities for sustainable retirement savings.

Citations

- 1.Retirement Benefits Act, Cap 197, Laws of Kenya.

- 2.Retirement Benefits (Occupational Retirement Benefits Schemes) Regulations, 2000.

- 3.Retirement Benefits (Individual Retirement Benefits Schemes) Regulations.

- 4.Retirement Benefits (Umbrella Retirement Benefits Schemes) Regulations.

- 5.Retirement Benefits (Umbrella Retirement Benefits Schemes) (Amendment) Regulations, 2020.

- 6.Retirement Benefits (Occupational Retirement Benefits Schemes) (Amendment) Regulations, 2021.

- 7.Retirement Benefits (Individual Retirement Benefits Schemes) (Amendment) Regulations, 2021.

- 8.National Social Security Fund Act, 2013.

- 9.Retirement Benefits Authority Industry Brief of December 2025.

- 10.Retirement Benefits Authority Industry Brief of December 2024.

- 11.Retirement Benefits Authority, "Kenya's Pension Assets rise to Ksh2.81 trillion in 2025", March 4, 2026.

- 12.Retirement Benefits Authority, "Securing Tomorrow: Key Findings on the State of Kenya's Retirement Benefits Sector", November 7, 2025.

- 13.ACTSERV, "The Emerging Trend of Pension Scheme Consolidation", (undated, but refers to 2023 data).

- 14.Cytonn Investments, "Progress of the Retirement Benefits Schemes in Kenya in Q1'2026", May 24, 2026.

- 15.Cytonn Investments, "Regulatory Changes in the Kenyan Pensions Industry", November 28, 2021.

- 16.National Social Security Fund, "Kenya's Pension Assets Quadruple in 10 Years", May 12, 2025.

How does this affect your business?

Get an AI analysis of this article grounded in your jurisdictions, practice areas, and any policy documents you've uploaded to Wansom.